IMPORTANT DISCLAIMERS:

Prophecy Asset Management Allegations: While Bloomberg News has confirmed that Brian Kahn is Co-Conspirator #2 in this DOJ document, and the SEC lawsuit against Hughes makes clear that Individual 2 is the head of the Vintage Capital Management LLC (Brian Kahn), we remind readers that to date Brian Kahn has not been accused of OR charged with any crime.

I am/we are short RILY. All information for this article was derived from publicly available information. Investors are encouraged to conduct their own due diligence into these factors. This article represents the opinion of the author as of the date of this article. The information set forth in this article does not constitute a recommendation to buy or sell any security. This article contains certain “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential,” “outlook,” “forecast,” “plan” and other similar terms. All are subject to various factors, any or all of which could cause actual events to differ materially from projected events. This article is based upon information reasonably available to the author and obtained from sources the author believes to be reliable; however, such information and sources cannot be guaranteed as to their accuracy or completeness. This article reflects the author’s opinion at the time of publication. The author makes no representation as to the accuracy or completeness of the information set forth in this article and undertakes no duty to update its contents. The author may also cover his/her short position at any point in time without providing notice. The author encourages all readers to do their own due diligence.

- This report looks at linkages and ties – including many we believe are undisclosed – between the sub-advisor at the center of the Prophecy Asset Management scandal (Brian Kahn) and his preferred source of financing (B. Riley)

- We have surfaced several loans between B. Riley and Brian Kahn – largely involving stock equity collateral – many of which were not disclosed in B. Riley financials or in the proxy filings for the FRG deal and that remain ongoing (see later in report)

- We found conclusive evidence that over the years, Kahn has pledged shares of BW, FRG, and SNCR to B. Riley, and most recently pledged his stake in Freedom VCM Holdings LLC to B. Riley (the entity through which Kahn owns Franchise Resource Group)

- Notably, B. Riley’s lending to Kahn appears to have commenced after Brian Kahn took down the entire $92.5mm break fee for the Rent-A-Center debacle (letting B. Riley off the hook despite their negligence in the transaction). B. Riley would have likely faced severe financial distress had it paid its share of the breakup fee and investors deserve to know if the loans were in any way related to the breakup fee.

- B. Riley also acquired a number of assets from Brian Kahn after he paid the $92.5 million break fee, all at prices that all look extremely high relative to current value

- Given the tight relationship between B. Riley and Kahn, and the fact that Kahn was consistently borrowing from B. Riley and selling assets to B. Riley, there is no excuse for how B. Riley “missed” the allegations of wrongdoing involving Kahn – it should have caught the allegations in its loan and manager due diligence as related civil litigation was public dating back to 2021

- As we show in this report, there are serious questions as to whether B. Riley is acquiring assets from Kahn as a form of “pay back” relating to an under the table agreement they struck after the botched Rent-a-Center deal, given that B. Riley has repeatedly ignored public red flags about Kahn, made loans to him without disclosing them, and acquired assets from him at obviously inflated values

- Even the private credit fund (Irradiant) that backed the FRG take-private has ties to B. Riley that were not properly disclosed to the market – Irradiant’s Chairman and Co-Founder was previously CEO of Core Scientific, a B. Riley backed crypto mining operation

- Investors in Irradiant, Prophecy, B. Riley, and Kahn’s funds need to immediately demand unbiased outside counsel investigations into B. Riley’s economic ties to Kahn, the circumstances surrounding the funding of the FRG deal, and whether reps/warranties made at close were in fact true.

Background on Prophecy Asset Management / Co-Conspirator 2

On November 2, 2023, John Hughes (former compliance officer for Prophecy Asset Management) entered a guilty plea in federal court for his role in a multi-year $294 million fraud at alleged “first-loss” fund Prophecy Asset Management. The guilty plea described two co-conspirators (coded in the documents as #1 and #2). Bloomberg confirmed that Co-Conspirator #2 is Brian Kahn, CEO of FRG. In its most recent 10Q, B. Riley claimed to have “invested” $281 million into a Brian Kahn led take private transaction involving FRG.

We suggest readers first read the parallel SEC complaint against the compliance officer for Prophecy as it is less redacted than other versions

Needless to say, the facts laid out by the government are an exceptionally bad look for Brian Kahn. The SEC’s complaint includes allegations that Kahn ran up enormous losses and covered them up, forged the signature of his underage son, tried to pass off fake collateral from companies he controlled, and took “loans” from Prophecy Asset Management that he never returned. Notably, Deloitte was the auditor for Prophecy Asset Management and according to the SEC complaint resigned from the audit around March 2020 due to concerns over fraud (para 10). Deloitte is also the auditor for FRG. While Co-conspirator #2’s role in Prophecy may not have been obvious back in March 2020, today we wonder whether Deloitte will reevaluate its ongoing audit role at FRG (which of course could have explosive results for the value of the highly levered equity that is already falling apart on a fundamental basis).

On the earnings call, B. Riley CEO Bryant Riley offered enthusiastic support of Brian Kahn, referencing an alleged statement (that no one seems to have seen), and stating that this mystery public statement from Kahn is “good enough” for him (alluding to their multi-year strong working relationship). Riley’s tone was flippant, defiant, and utterly unbecoming of a public company CEO with responsibilities to outside shareholders. It is telling that B. Riley did not immediately engage outside counsel to conduct a special investigation regarding B. Riley’s business dealings with Kahn.

If B. Riley really only found out about the Kahn allegations after the Hughes guilty plea in November 2023 (as Bryant Riley claimed on the earnings call), then the firm lacks basic due diligence capabilities. This article from February 2021 went into great detail about Kahn’s problems and point to civil litigation that had already been filed by that time. And as we show in this article, B. Riley has repeatedly transacted with – and lent money to – Brian Kahn since these allegations surfaced, requiring the firm to undertake diligence efforts.

It is implausible that B. Riley missed all these serious allegations about Kahn. It therefore seems more likely that B. Riley as a firm has chosen to ignore red flags it sees with Kahn. This wanton disregard for risk management is likely to lead to the ultimate demise of the firm.

Timeline of Kahn’s Dealings with B. Riley vs. Allegations from the SEC Complaint

Using the SEC complaint and other public documents, we have attempted to tie together the industrial logic of transactions between B. Riley and Brian Kahn to get to the bottom of what is really going on between B. Riley and Brian Kahn and why B. Riley magnificently overpaid to participate in the management buyout of Franchise Resource Group.

Summer/Fall 2018 – BW Rescue

We believe the excerpt below from the SEC points to a transaction Kahn did with BW (the company that recently imploded):

The SEC complaint references a troubled company in which Vintage was heavily invested in 2018. We believe that company is Babock & Wilcox (BW). In August 9, 2018, BW announced a $30 million financing from Vintage that was a form of rescue financing. The relative size of the Prophecy “loan” and the timing and description of the investment seem to match with BW. By 2018, Vintage was a large holder of BW and the company had gotten into financial trouble. Notably, despite having a “loan” from Prophecy and presumably having more than enough cash on hand, B. Riley backstopped Kahn’s $30 million investment. If Vintage had the money and knew it was money good, it is surprising that B. Riley would step up and backstop the transaction at this time.

Source: BW Release

Source: BW Release

This begs the question of whether B. Riley knew Vintage was having money troubles by August 2018 stemming from the problems at Prophecy. As alleged in the complaint, rather than paying back the “loan” from Prophecy above, Kahn appears to have just kept the money and assisted Prophecy Asset Management with covering up the loan non-payment by accepting wires of NEW money from Prophecy Asset Management into other accounts he controlled and then eventually wiring that money back to Prophecy via his Vintage funds to create the appearance that the loan was paid off. These allegations are outlined in the SEC complaint.

December 2018 through April 2019 – Vintage Owes the $92.5MM RCII Break Fee

Kahn had another much larger need for cash that emerged in December 2018 through March 2019. As he was hemorrhaging money in the Prophecy Asset Management trading accounts, Kahn and B. Riley together lost a $126.5 million verdict for failing to fill out paperwork on time and triggering the break fee clause in their joint and now failed acquisition of Rent-A-Center. Bloomberg’s Matt Levine did a great piece on this story here so we won’t waste time on it.

After losing in court, Kahn, B. Riley and Rent-a-Center came to a settlement agreement and Kahn took the entire burden of the legal fee down on his own, absolving B. Riley of its ~$34 million share. Rent-a-Center agreed to this smaller total break fee. This resulted in Kahn owing $92.5 million by May 23, 2023 and kept B. Riley out of financial distress.

What’s amazing about this figure is that we know Kahn was bleeding money at Prophecy Asset Management and owed huge amounts of money back to Prophecy. Yet despite being underwater at Prophecy, it appears that Kahn made good on paying the $92.5 million fee on time because there were no court filings suggesting he didn’t.

How did Kahn finance the fee? Where did he get the money from? Did any of the $92.5 million break fee get paid out of money he pulled from Prophecy Asset Management?

And most importantly, after being “absolved” from the fee, did B. Riley go on to finance it?

April 2019 – June 2019 Kahn Allegedly Tries to Pass off Fake Buddy’s Certificates

According to the SEC complaint, between April 2019 and June 2019 – the period during which Kahn settled and agreed to pay the $92.5 mil break fee to RCII – he simultaneously began allegedly fabricating documents to pledge collateral to Prophecy Asset Management worth somewhere north of $200 million to fix his trading loss hole. According to the complaint, the fabricated collateral was in the form of fake preferred stock certificates in Buddy’s Home Furnishing. Buddy’s was a private company that Kahn owned at the time (this business would later get sold into the public company FRG).

It makes sense that Kahn felt the cash crunch by this time given that he had just agreed to an enormous settlement and was continuing to lose money in his Prophecy accounts. Therefore, his alleged need to paper over the losses with fake certificates makes sense in the timeline.

What happens next is not reported in the SEC document. We cannot understand how or why B. Riley began to step up and loan Kahn money against his holdings. However, we scoured UCC filings across the country and the record is clear and undeniable – Kahn began to borrow extensively from B. Riley immediately after he paid the break fee to RCII. We found evidence that only some of these loans have been disclosed to the public.

July 2019 – BW Margin Loan

On July 29, 2019, Brian Kahn pledged 5 million shares of BW to B. Riley in exchange for a loan. This SEC filing from BW includes the 5mm share pledge.

Importantly, we were able to replicate this finding using UCC searches. The document below makes clear that 5mm shares were pledged by Vintage to the benefit of B. Riley around July 24, 2019, corresponding with the entry above:

The fact that this UCC filing ties out to an actual margin loan is pivotal for the rest of this piece, as it establishes that margin loans take the form of a UCC filing with a lien. In this case, the loan was publicly disclosed. Later loans appear to have been made without public disclosure.

July 1, 2020 – Secured Loan to Kahn Entities Against FRG Related Shares

We confirmed that an entity using the name “Stefac LP” is controlled by Brian Kahn. The address lists to the same address as Kahn, and this filing confirms that Kahn is behind the Stefac LP entity. Below, Kahn pledged 2mm shares of FRG to B. Riley in 2020 (yes, the business RILY just acquired with Kahn) to RILY.

At this point, it seems like RILY loans to Kahn were going up in size. A 2mm share pledge at that time would have represented around $40 million worth of stock pledge give or take as FRG traded around $20/sh back then.

From Delaware UCC filings we found, it appears the Stefac LP pledge was terminated by August 2020, suggesting the loan was only short duration in nature. However, it was not the last loan that the company made to Kahn against his FRG shares.

Nov 2020 – B. Riley Forces Bebe to Acquire Assets from Kahn

We previously wrote about BEBE and we believe that our report likely forced B. Riley to buy BEBE in and consolidate it. B. Riley very clearly controlled BEBE but postured publicly that Manny Mashouf – a man in his 80s with no experience in the subprime furniture business – was actually running the company.

In November 2020, B. Riley and one of the company’s largest shareholders (Neil Subin) provided financing to BEBE so it could acquire 47 Buddy’s stores from Kahn’s FRG (from the subsidiary Buddy’s Home Furnishing that was the subject of the aforementioned allegedly fabricated collateral). While it is hard to tell whether the purchase price was fair, we note that BEBE’s stock price has been a straight line down since that point (RILY came in at $5/sh to finance these purchases and the latest trading price of BEBE is $3/sh). This looks like a value transfer from B. Riley shareholders to Kahn.

Feb 2021 – Kahn Dumps His Floundering BW Shares on B. Riley

It was at this point in the timeline that the “value transfer” from B. Riley to Kahn seemed to accelerate.

BW recently blew up, falling over 50% on Friday November 10th. But importantly, the stock has obviously been languishing for years (keep in mind Kahn was doing rescue financings into it back in 2018 as mentioned earlier).

In February 2021, Kahn sold 10.7mm shares of BW to B. Riley. As a result of this and other transactions, B. Riley became the controlling entity of BW holding around 31% of all shares. It appears that B. Riley acquired the shares from Kahn for $6/sh. The stock is $1 today. This looks like an egregious transfer of wealth to Kahn, who walked away with around $60mm for a business that was very obviously dying. Had he held on, his stake would be worth around only $10mm today. One has to wonder what economic logic guided the B. Riley decision to “clean Kahn out” of his BW shares given what has transpired in BW since 2021.

June 2021 – Nomura Agreement Suggests B. Riley Owns Economics in Kahn’s Fund Vintage

On page 33 of the June 2021 credit agreement between B. Riley and Nomura, we found out that B. Riley carved in language to adjust its covenant-relevant earnings for advisory fees related to Vintage Management Capital, LLC. A Google Search for this specific name returns only B. Riley’s credit agreement and no sign of this legal entity. We therefore believe that the naming was a typo, and that the fund in question here is “Vintage Capital Management LLC” (Kahn’s hedge fund). B. Riley has a capital raising business where it charges hedge funds a fee to raise money. We interpret this commentary to mean that B. Riley had some capital introduction economics associated with Kahn’s hedge fund Vintage. It appeared significant enough to warrant a call out in the earnings add back math.

Given that Vintage is named in the SEC complaint regarding Prophecy, if B. Riley does have economics in this entity, it should be disclosing much more information about its ties with Kahn to the public.

For example: Did B. Riley push its wealth management clients into Kahn’s funds? This should be disclosed and an internal investigation should immediately be commissioned to explore this topic.

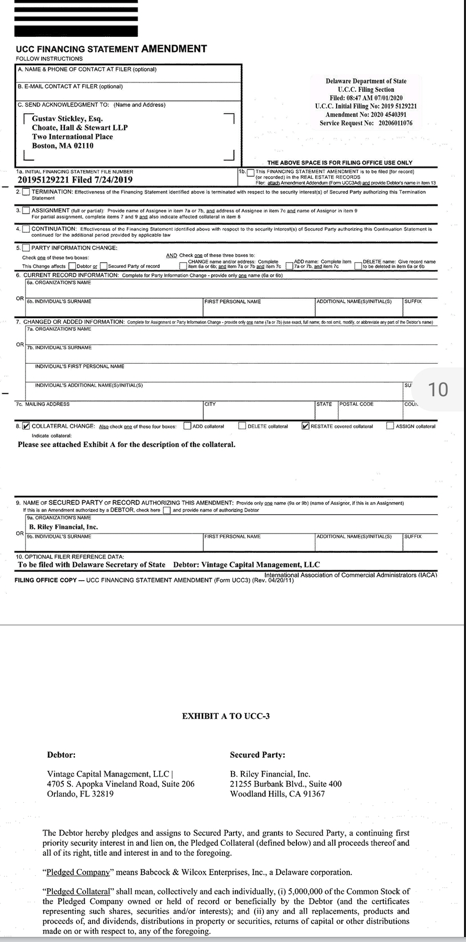

Jan 2023 – Kahn Pledges his FRG, SNCR, and Wells Fargo Account to B. Riley

From Florida UCC filings, we determined that Kahn pledged his FRG shares, his SNCR shares (we did not even know he owned SNCR), and a Wells Fargo securities account to the benefit of B. Riley in January 2023. See below:

The language in this pledge is expansive and appears to include all of Kahn’s holdings of FRG. This is important because this stock pledge (and any associated loan) was never mentioned in the proxy filing for the FRG deal. It makes no sense why RILY would have such an all-encompassing pledge from Kahn unless they had a loan out to Kahn against his holdings (this is the entire purpose of creating a UCC filing as we established in the earlier and disclosed BW margin loan).

On page 43 the proxy details that the fairness opinion value for FRG came in well below $30. In other words, B. Riley massively overpaid for FRG according to its own paid for analysis. One has to therefore wonder whether B. Riley made a margin loan to Brian Kahn that was upside down and did not want to recognize the loss, deciding it might be better to just take the company private at an inflated mark. While this is speculation on our part, it is hard to understand what happened here and B. Riley owes it to investors to explain why the bank had a security pledge including FRG from Kahn right ahead of buying the business.

Investors should also ask questions about why B. Riley took a security pledge of SNCR – a literal penny stock that was charged with fraud by the SEC just six months before this pledge. What kind of bank lends against a $1 stock, let alone one charged with fraud?

Perhaps the same type of bank that makes a non-binding buyout offer that never goes anywhere for the exact same penny stock but then does not actually go forward with the buyout. Yes – not even two months after securing this SNCR pledge from Kahn, B. Riley put in what appears to have been a fake offer for SNCR at a $1.15 share price. The stock is in the 40 cent range today.

The January 2023 pledge was terminated in August 2023 (see below). However, that is not the end of the pledge story.

August 21, 2023 – Same Day FRG Take-Private Closes, Kahn Enters into New Pledge Agreement

Per this 8K, the FRG deal closed on August 21, 2023. On the very same day, the UCC lien above seems to have been replaced with a new UCC lien that involves Kahn pledging “Freedom VCM Holdings, LLC” along with SNCR (a penny stock also owned by B. Riley) to B. Riley. Freedom VCM Holdings is Kahn’s stake in private FRG (it is the company that now holds FRG). Again, the only reason Kahn would pledge his private stake in FRG to the benefit of RILY is if he is borrowing money from RILY. The very fact that the UCC collateral was rolled from the public company FRG to the private entity Freedom suggests there is an active loan against Kahn’s collateral, hence the UCC required a “refresh”. So RILY appears to have a loan to Kahn that exists at the very present moment against Kahn’s stock in the private Franchise Resource Group.

Does B. Riley therefore have far more exposure to this deal than they are letting on to the market? The deal obviously looks like a bust for a number of reasons – between the awful fundamental performance since the acquisition was announced, as well as the “management issues” that are lurking in the shadows. It is time for B. Riley to start coming clean with investors about its dealings with Kahn, its loans to Kahn, and any other economic relationships it has to Kahn outside of the FRG deal.

Other Red Flag in Private Credit Financing – Irradiant Capital Ties to B. Riley

One immediate red flag that struck us when the FRG deal was announced is that the private credit fund backing the deal with $475 million – Irradiant Capital – is Chaired by Michael Levitt. Michael Levitt is the Chairman and Co-Founder of Irradiant Partners but is also the former CEO and current large shareholder of Core Scientific, a bitcoin mining stock that counted as one of its largest financiers B. Riley. In fact, in February and March of 2023, at the very same time that B. Riley was negotiating its deal to acquire FRG, it was also making a $70MM DIP loan to bankrupt at the time Core Scientific. According to Bloomberg, Levitt of Irradiant personally owns 22.6mm shares of CORZQ which continues to trade. So, B. Riley was funneling new money into Levitt’s company at the same time that Levitt was about to funnel money into B. Riley’s acquisition of FRG. We are surprised that the obvious conflict of interest here was not more clearly disclosed.

Conclusion

Brian Kahn appears to have gotten very upside down starting in 2019 thanks to his trading problems at Prophecy and the big break fee from the Rent-a-Center deal. As soon as he got upside down, it appears that B. Riley stepped up and started financing him with margin loans and also by buying assets from him at inflated levels (BW, Buddy’s through BEBE, and FRG).

In our view, B. Riley disregards its minority shareholders and manages itself as if it were private. This governance misalignment is now proving to be costly. B. Riley is burdened with years of economic entanglement with Brian Kahn, an individual who is clearly facing trying times ahead.

B. Riley is over-levered, its investments are atrocious, and it has been bleeding economic value to high level insiders via an unsupported dividend, as well as to “friends of the firm” through non-economic dealings. We expect the end game for this stock to be extremely ugly – one for the history books.

It also turns out Kahn is not the only person who loves excessive leverage. Mr. Riley appears to have made an expansive and exhaustive pledge of personal assets (including his personal stock holdings) to Axos Bank (a regional bank that has a penchant for the same “types” of customers and business relationships as B. Riley):